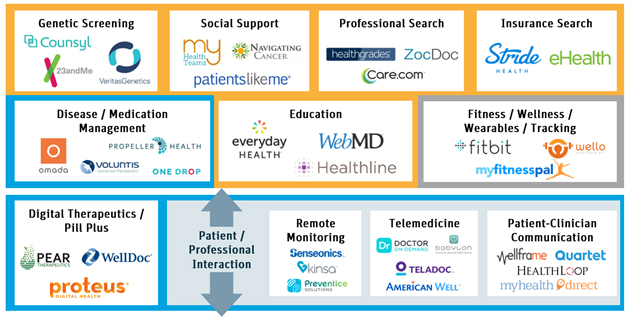

Winter 2017 Consumer Digital Health: Market Shift Is Leading to New Opportunities By Steve Allan, CFA, Head of SVB Analytics, and Alex Lee, Manager, Life Science and Digital Health, SVB Analytics The newest wave of consumer digital health investment focuses on applications encouraging consumers to change health-related behaviors, shifting from fitness/wellness to clinically driven solutions that lead to better health outcomes at lower costs. This trend underscores why there are greater opportunities for companies with technologies that create value for payers, providers, employers, and consumers. SVB Analytics examined these trends in a recent report, Consumer Digital Health: Market Shift Is Leading to New Opportunities. Below is a summary of the reports highlights. Where in Consumer Digital Health Are Investors Focused? Since 2011, investment in the digital health ecosystem has nearly quadrupled, with about half of the number of digital health investments made in companies with technologies that interface with the consumer. This reflects the convergence of technologies to drive and measure improved health outcomes and cost savings—and funding is following. Consumer digital health, mapped in the chart below, includes a wide variety of products and services, from diabetes management applications to telemedicine services to platforms that help consumers find a doctor. In 2015, more than $2.5 billion was invested in the sector, compared to roughly $0.5 billion in 2011.

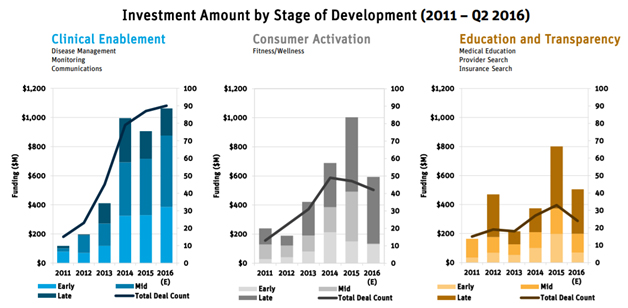

The advent of the quantified-self movement in the early 2010s attracted significant capital, especially in the fitness/wellness category. Today, the targets of consumer digital health financing have changed. Investors are shifting from health insurance and provider search, as well as medical education and fitness/wellness applications, to more clinically focused areas. This focus includes disease management, remote monitoring, and patient-provider communications (outlined in blue in the chart above). Notably, the percentage of investment dollars allocated to clinically focused companies grew from 22 percent in 2011 to 49 percent in Q2 2016. These companies are also seeing growth in early-stage funding: Early-stage financing for clinically focused companies quadrupled from $79 million to $329 million in the same period. By comparison, investments in consumer activation and the education and transparency segments have declined. What Are the Best Clinical Application Opportunities? Clinically focused areas of disease management and patient provider communications are seeing the largest increase in early-stage funding, indicating new start-up formation. At the same time, consumer activation companies and education and transparency companies are maturing with fewer early-stage rounds raised.

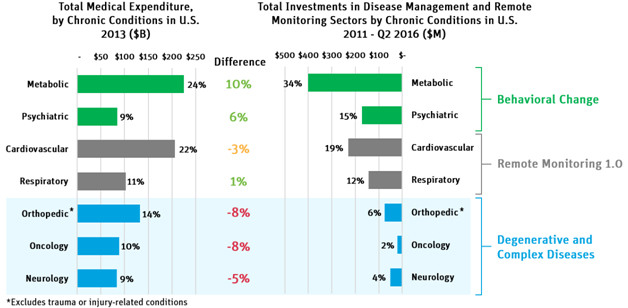

* (E) represents estimated value. This is calculated by doubling the data from the first half of 2016. Looking ahead, degenerative and complex diseases, which are difficult to manage and account for a significant portion of U.S. medical expenditures, have received comparatively lower digital health investment, signaling the space is ripe for disruption.

Since 2011, nearly half of the clinically focused investments have been made in behavioral change technologies (such as treating metabolic or psychiatric conditions). However, only 12 percent of investments have been made in companies focusing on degenerative and complex diseases (such as treating orthopedic, oncologic, and neurologic conditions). Yet in 2013, 33 percent of all medical expenditures were made in this segment. This suggests a potentially lucrative opportunity for technologies developed to treat these diseases, given the novelty of the area and lack of cost-effective solutions to manage them. What Does the Future Hold for Digital Health Investing? As investors move toward more clinically focused strategies, wearables and wellness companies are executing different strategies to adapt to this shifting landscape, including seeking acquirers and partners. Going forward, as digital health companies create new solutions that target expensive and hard-to-manage diseases, we expect to see improved integration of hardware and software. As these solutions become more clinically focused, we envision the need for growing coordination with payers, providers, and regulatory bodies. We also anticipate bigger investment opportunities in technologies that provide quantifiably positive health outcomes at lower costs.

For more information, please see the full SVB Analytics Consumer Digital Health Report. For more about SVB Analytics, please visit our website.

Disclosures SVB Analytics is a member of SVB Financial Group and a non-bank affiliate of Silicon Valley Bank. Products and services offered by SVB Analytics are not FDIC insured and are not deposits or other obligations of Silicon Valley Bank. SVB Analytics does not provide investment, tax, or legal advice. Please consult your investment, tax, or legal advisors for such guidance. ©2016 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of the FDIC and the Federal Reserve System. Silicon Valley Bank is the California bank subsidiary of SVB Financial Group (Nasdaq: SIVB). SVB, SVB FINANCIAL GROUP, SILICON VALLEY BANK, MAKE NEXT HAPPEN NOW, and the chevron device are trademarks of SVB Financial Group, used under license. Non-Dilutive Funding Sources for Medical Device and Biotechnology Companies By Andrew Ellis, Associate (Palo Alto) Readers of The Life Sciences Report are not strangers to the idea that securing investors for medical device and biotechnology companies is never easy. Anecdotal reports from our clients indicate that investors at every stage want more product or process advancement prior to a new investment than they did in past years. Although total dollars invested in the life sciences industries have increased over the last several years, the MoneyTree Report from PricewaterhouseCoopers for the third quarter of 2016 showed a decline of 17 percent by value and 26 percent by volume on a year-over-year basis.1 Whether or not that decline becomes a trend in 2017 is uncertain, but to help combat any potential fundraising headwinds, companies would benefit from examining (or re-examining) non-dilutive sources of funding to further advance product development and regulatory processes before their next investor pitch. What Are the Benefits of Non-Dilutive Funding? There are several benefits to obtaining non-dilutive funds, the most obvious of which is that such funds are not given in exchange for an equity stake, so founders are able to retain more voting control of the company. More relevant to companies preparing to raise money from venture capital is that the product or idea could be more mature and de-risked prior to fundraising because of the non-dilutive funds the company received. Utilizing these funds also shows potential investors that the company is resourceful and can accomplish a lot with its invested dollars. Finally, depending on the source of the funds, the company may also find advisors and partners that can help the company through their guidance and connections going forward. When Should I Look into Non-Dilutive Funding? It is really never too early to begin looking into potential sources of non-dilutive funding. In fact, non-dilutive funding can start before company formation for some companies. For example, research conducted in an academic setting can utilize basic research grants to de-risk a technology before the company is formed or help define the breadth of the future offering. Another benefit to addressing this issue prior to company formation is that certain government grants, such as specific National Institutes of Health (NIH) grants, can only be made to researchers or academic centers and not to companies. However, there are two primary risks to consider regarding this pre-formation approach. First, in the academic setting, researchers will need to work with the centers technology transfer office to help ensure that they will be the one to eventually benefit from this grant money and effort. Second, researchers must pay close attention to the terms and limitations attached to the funds, especially as they relate to intellectual property and the use of funds. For the vast majority of readers who have already founded companies, there is also good news for you: it is almost never too late to be looking into sources of non-dilutive funding. Many funding sources are aimed at commercializing technologies or assisting early- and mid-stage companies during their development processes. Especially in the case of the NIH and other government sources, even large, multibillion-dollar companies apply for and obtain non-dilutive funding for certain research and development initiatives. What Sources of Non-Dilutive Funding Are Available? There are many sources of non-dilutive funding from state and federal governments, foundations, and private entities. A few of the most common categories and sources are listed below.

The above represents only a few of the many sources of non-dilutive funding that are available to companies. If you would like to discuss any of the above issues further or need assistance structuring a financing of any type, please feel free to contact a member of Wilson Sonsini Goodrich & Rosatis life sciences practice.

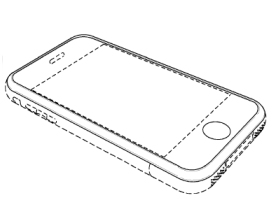

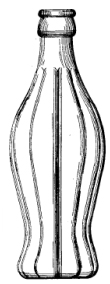

1 The MoneyTree Report for the third quarter of 2016 is available at http://pwchealth.com/cgi-local/hregister.cgi/reg/pwc-pharma-life-sciences-money-tree-q3-2016.pdf. 2 More information is available at https://grants.nih.gov/grants/oer.htm. 3 More information is available at https://sbir.nih.gov/funding. 4 More information is available at http://www.darpa.mil. 5 More information is available at http://cdmrp.army.mil. 6 More information is available at https://www.michaeljfox.org/research/apply-for-grant.html?navid=funding-opps. 7 More information is available at http://grandchallenges.org. 8 More information is available at http://www.gatesfoundation.org/How-We-Work/General-Information/Grant-Seeking-Resources. 9 More information is available at http://ww5.komen.org/ResearchGrants/FundingOpportunities.html. 10 More information is available at http://grantcenter.jdrf.org. 11 More information is available at https://www.cff.org/Our-Research/For-Researchers/Research-Awards/. 12 More information is available at http://www.xprize.org/prizes. 13 For examples of grants and tax credits, see https://ventures.jhu.edu/tedco-gives-four-200k-grants-to-local-life-sciences-companies/ and http://califesciences.org/connect2ca/incentives/state-incentives/, respectively. 14 For example, see http://onestart.co/about. 15 For example, see http://www.fogartyinstitute.org/innovation-faq.php. 16 For example, see http://www.childrensinnovations.org/Pages/TechnologyDevelopmentFund/ProofofConceptGrant.aspx. 17 For example, see http://www.nycedc.com/industry/life-sciences. 18 More information is available at http://medtechinnovator.org. 19 Our 25th Annual Medical Device Conference is on Friday, June 2, 2017, at the Palace Hotel in San Francisco. For more information, please contact Michelle Watkins at mnwatkins@wsgr.com. Utility Models and Design Patents: What You Should Know By Darby Chan, Associate (Palo Alto), and Doug Portnow, Partner (Palo Alto) Most inventors are aware of the importance of filing utility patent applications, through which protection of devices, methods, compounds, software, and so on is pursued and obtained. While there are many advantages to utility patent applications, there are also other types of patent applications that can provide a different set of advantages for protecting an invention. Two such commonly overlooked types of patent applications are utility models and design patents. Utility Model Patents Utility model patents protect the structure and/or function of an invention much like traditional utility patents. They are more quickly and less stringently examined, often only needing to undergo a registration-like process. In exchange for faster examination and issuance, patent term is much shorter, and while utility models are available in many important international markets, they are not available in the U.S. Despite these limitations, utility model patents remain very powerful in specific circumstances. While not available in the U.S., utility model patents are available in key international markets such as Australia, China, France, Germany, Italy, Japan, and Korea. If significant commercial activity (e.g., product development, sales, and manufacturing) is anticipated in these countries, utility model patent filings may be worth considering. Because a key advantage of the utility model is a short examination process, such filings should be considered particularly if the commercial activity is ongoing or anticipated shortly and enforceable patent rights are desired sooner rather than later. In terms of content, the requirements for utility model patents and traditional patents are essentially the same. There needs to be a written description of the invention, accompanying drawings, and a set of claims that define the legal right of the patent. Hence, the cost of preparing the utility model filing is often in the same range as the cost for a traditional utility patent application—$15,000 to $25,000. However, rather than undergoing a lengthy and stringent examination process as with utility patent applications, utility model patent applications are more loosely examined and typically undergo only a registration-like process. With lower costs of examination, the aggregate cost of obtaining a utility model patent is much less—low five figures or less versus mid-to-high five figures or more (in U.S. dollars). Once a utility model patent is obtained, it can be enforced for approximately the next six to fifteen years, depending on where it was granted and the amount of time examination had required. The patent term available is much less than the typical 20 years available from utility patents. Therefore, utility model patents may not be appropriate for inventions where longer patent term is important, such as biopharmaceuticals and significant medical innovations. On the other hand, the lower cost, quicker examination, and shorter patent term may be justified for incremental innovations, such as improvements to manufacturing processes and ancillary features in products and processes, or for industries where product cycles are very short. There are also differences in the enforcement of utility model patents and utility patents. Because utility patents have undergone a lengthy and stringent examination process, they are presumed valid. And, the alleged infringer of the patent has the burden of showing that the patent is invalid. This concept does not apply completely to utility model patents. If an owner of a utility model patent sues an alleged infringer, they typically will have the burden of proving that the invention protected is novel, non-obvious, and therefore patentable. In other words, the burden and costs of establishing patentability for utility model patents are back-loaded but optional in a sense. As a result, it is often recommended that inventors and their patent counsel carefully research and evaluate the merits of their invention prior to the initial preparation and filing of a utility model patent application. The table below summarizes some of the key aspects of a utility model. Design Patents Design patents are patents that protect the appearance or ornamental design of an object. Some well-known examples are the Apple iPhone in Figure 1 below and the Coca-Cola contour bottle in Figure 2 below.

Figure 1: Apple iPhone, U.S. Design Patent No. D593,087

Figure 2: Coca-Cola contour bottle, U.S. Design Patent No. D48,160 It is important to emphasize that a design patent only protects the aesthetics of the design, and not any of the functional aspects of an invention. An example of this might be a new aerodynamically shaped component of an aircraft. Because the shape of this component was designed for aerodynamic purposes, it is functional and therefore would not be protectable with a design patent. On the other hand, the shape of the Coca-Cola contour bottle was designed for aesthetic reasons, not functional reasons, and therefore the bottle was patentable. Functional aspects are protected with a traditional utility patent application or a utility model patent. Thus, if the shape or look of the product is related to a functional aspect, a design patent cannot be pursued. The United States and many other jurisdictions such as China, Japan, South Korea, Europe, Canada, and South Africa provide for design patents. Design patents often can be obtained faster and at significantly less cost than traditional utility patents. For example, in the United States, a design patent may be obtained in approximately one to two years, and the cost for filing the application may range from about $3,000 to $5,000, with the majority of the cost coming from obtaining high-quality illustrations of the various views of the product. This amount is in contrast to the $15,000 to $25,000 it may cost to prepare and file a traditional utility patent. Examination of a design patent is typically based on novelty and non-obviousness of the design. Infringement of a design patent in the United States is based on whether an ordinary observer believes that the allegedly infringing design is substantially the same as the patented design. Therefore, design patents generally provide protection against knock-off products, but a competitor may make simple ornamental feature changes in order to easily get around a design patent. As a result, protection can be somewhat limited. Nevertheless, historically a design patent still could be a powerful form of protection because damages were calculated differently than in a utility patent infringement case. Until recently, damages in a design patent case were based on the entire profits of the infringing design, as opposed to only a portion of the profits that are covered by an invention in a utility patent infringement case. As an example, Apple was previously awarded approximately $400 million in a lawsuit with Samsung based on the enforcement of several design patents. However, just recently, the U.S. Supreme Court rejected this traditional view of design patent damages, and the Samsung award was tossed out. The Supreme Court ruled that damages may be based on individual components covered by a design patent rather than the entire product. The Court failed to provide further specifics on the issue, and it will now take additional court rulings to clarify the ambiguity. While these factors certainly are in favor of filing design patents, it is important to note that the term of a design patent is typically shorter than that of a utility patent. For example, in the United States, a design patent is valid for 14 or 15 years from the time of grant, depending on when it was filed. In other countries, a design patent may be valid for as short as five years and as long as 25 years. The preparation of a design patent is fairly straightforward. A design patent application includes a single claim and a series of drawings to show the various views of the design (e.g., top, bottom, sides, and perspective). In the United States, there is a six-month grace period to file a design patent after a public disclosure, but an inventor should not rely on this grace period since it may not be applicable in foreign jurisdictions. In sum, inventors should consider pursuing design patents in order to protect the ornamental features of their designs. Design patents can be obtained relatively quickly and at lower cost than traditional utility patents. While design patents potentially may provide less protection than utility patent applications, damages can be significantly higher. Inventors should therefore consider both utility patent applications to protect the functional aspects of their invention and design patents to protect the ornamental features of their invention. The table below summarizes some of the key features of a design patent. Conclusion Inventors and businesses should consult with their legal counsel to determine the commercially significant aspects of their innovations, discuss market entry and commercial partnership strategies, and ultimately align their patent filing strategy with these business needs. Utility model patents and design patents may be considered in addition to utility patents, and the countries that are selected for patent filings should be carefully considered as well.

Effective Regulatory Strategies: Tapping into FDA Expedited Review Programs By David Hoffmeister, Partner (Palo Alto), and Charles Andres, Associate (Washington, D.C.) Effective regulatory strategies are important success drivers for drug and medical device companies. They have several components and:

In this article, we provide an introduction to four important FDA programs that are designed to help expedite drug and medical device development and market entry.1 These programs should always be evaluated when designing effective regulatory strategies. Fast Track Designation (Applies to Drugs) There are two ways for a drug to qualify for Fast Track designation: (1) a drug candidate must be intended to treat a serious medical condition and have associated data (clinical or non-clinical) that demonstrates the drugs potential to address an unmet medical need, or (2) a drug candidate must have been designated as a qualified infectious disease product (QIDP).2 Fast Track designation comes with several advantages, including frequent interactions with the FDAs designated product review team to discuss clinical study design, dose-response concerns, biomarker use, and the extent of data required to show safety for the drug candidate. Based on a preliminary evaluation of clinical data, the FDA may additionally determine that the drug candidate is eligible for Priority Review (see below discussion). For the period 1998-2010, approximately 36 Fast Track-designated drugs were approved in the FDAs Center for Drug Evaluation and Research (CDER).3 Included among these approvals are the drugs darunavir (for treating AIDS), sorafenib tosylate (for treating renal cell carcinoma), and levofloxacin (for treating post-inhalation anthrax exposure).4 Based on their clinical data, Fast Track-designated drugs may also be eligible for rolling review—where the FDA reviews each section of a non-disclosure agreement (NDA) or biologics license application (BLA) as it is ready—rather than waiting for the whole NDA or BLA to be assembled and submitted. Fast Track designation does not change the standard required for approval, which is substantial evidence of safety and effectiveness from two Phase 3 well-controlled clinical trials, or one large, well-controlled Phase 3 study (usually reserved for biological products). Priority Review Program (Applies to Drugs) Similar to the Fast Track Program, a drug candidate may quality for Priority Review, under which the FDA sets the target date for FDA action on an NDA or BLA at six months after the FDA accepts the application for filing. Priority Review is granted when there is evidence that the drug candidate would be a significant improvement in the safety or effectiveness of the treatment, diagnosis, or prevention of a serious condition. If criteria are not met for Priority Review, the application is subject to the standard FDA review period of 10 months after the FDA accepts the application for filing. Priority Review designation does not change the scientific/medical standard for approval or the quality of the evidence necessary to support approval. In 2015, 24 novel drugs approved by the FDA were given Priority Review.5 These drugs included alectinib (for treating non-small cell lung cancer) and eftazidime/avibactam (a fixed-dose combination drug containing a novel non-β-lactam β-lactamase inhibitor for treating bacterial infections). 6,7 Accelerated Approval Program (Applies to Drugs) To qualify for the Accelerated Approval Program, a drug candidate must treat a serious or life-threatening disease or condition and such treatment must provide a meaningful advantage over available therapy. Drugs approved under the Accelerated Approval Program are conditionally approved by the FDA based on surrogate endpoint, which is an endpoint that is considered reasonably likely to predict clinical benefit or a clinical endpoint that can be measured earlier than irreversible morbidity or mortality (IMM) that is reasonably likely to predict an effect on IMM or other clinical benefit.8 An example of a surrogate endpoint for a cancer drug candidate would be a reduction in tumor mass or volume. For drugs granted Accelerated Approval, post-marketing clinical trials (Phase IV trials) are required to be completed with due diligence to show drug effect on IMM or other clinical benefit. The FDA may withdraw approval of an Accelerated Approval drug if the post-marketing trials fail to verify the expected effect on IMM or expected clinical trial benefit. According to one study, five drugs were withdrawn over the period 2005-2011 after having been approved as Accelerated Approval drugs.9 Drugs approved under the Accelerated Approval Program in 2015 include venetoclax (a small-molecule drug for treating chronic lymphocytic leukemia in a specific patient population) and atezolizumab (an anti-cancer antibody).10 Breakthrough Therapy Designation (Applies to Both Drugs and Medical Devices) In order to qualify as a Breakthrough Therapy drug candidate, a product must demonstrate preliminary clinical evidence (alone or in combination with other drugs) of substantial improvement over existing therapies on one or more clinically significant endpoints. After receiving the request, the FDA has 60 calendar days to either grant or deny the request. A Breakthrough Therapy designation conveys all of the Fast Track Program features, provides more intensive FDA personnel interaction, and includes an organizational commitment by the FDA to involve its senior management in the development program, and eligibility for rolling and Priority Review. Specifically, the following actions, where appropriate, are required by the agency:

Drugs approved under Breakthrough Therapy designation in 2016 include nivolumab (an anti-cancer antibody) and atezolizumab (an anti-cancer antibody checkpoint inhibitor).11 With President Obamas signing of the 21st Century Cures Act into law in December 2016, medical devices are also eligible for Breakthrough designation. Section 3051 of the act creates priority review for Breakthrough-designated12 medical devices. To qualify, a medical device must: (1) provide for more effective treatment or diagnosis13 of a life-threating or irreversibly debilitating human disease or condition, and (2) represent a breakthrough technology: (a) for which no approved or cleared alternatives exist; (b) that offers significant advantages over existing approved or cleared alternatives;14 or (c) where availability of the device is in the best interests of patients. These qualification criteria give the FDA broad latitude in assigning Breakthrough designation. Breakthrough designation for medical devices comes with a variety of benefits, including: assigning an experienced FDA team to the review, providing for team oversight by senior agency personnel, adopting efficient processes for timely dispute resolution, and providing for timely, interactive communication with the FDA during device development and review. Conclusion Today more than ever, it is important that drug and medical device developers craft efficient and effective regulatory strategies. An important part of this process is to properly utilize FDA programs for expediting development and approval.

1 The FDA has issued guidance for these four expedited programs. See http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/ 2 QIDP designation comes out of the Generating Antibiotic Incentives Now Act (The GAIN Act). The GAIN Act incentivizes the development of antibiotics and recites specific strains of bacteria. If an antibiotic in development targets one of the recited bacterial strains, the antibiotic can get QIDP designation. However, designation is not limited to drugs targeting these bacterial strains. Thus, if a company is developing an antibiotic or antiviral drug, it is worth determining whether the drug can be QIDP designated and therefore automatically put on the FDAs Fast Track. 3 See http://www.fda.gov/downloads/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ 5 See http://www.fda.gov/Drugs/DevelopmentApprovalProcess/DrugInnovation/ucm474696.htm. A small number of these drugs were granted Priority Review through redemption of a Priority Review voucher and thus may have been exempt from the requirement to provide a significant advance. 7 Fixed-dose combination drugs containing a novel active ingredient (i.e., an active ingredient not previously approved under the Federal Food, Drug, and Cosmetic Act (FDCA)) are now eligible for new chemical entity (NCE) five-year FDA regulatory exclusivity upon FDA approval. 8 See http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/guidances/ucm358301.pdf. 9 See http://www.valueinhealthjournal.com/article/S1098-3015(14)00137-5/abstract. 10 See http://www.fda.gov/downloads/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ 11 See http://www.fda.gov/downloads/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ 12 Designation requests may be made before application submission, notification, or a petition for classification. The act specifies that the FDA should make a designation determination no later than 60 days after submission of a request. 13 510(k), de novo, and premarket approval devices may be eligible for Breakthrough designation and Priority Review. 14 Significant advantages can include: reducing or eliminating hospitalization; improving patient quality of life; facilitating patients ability to manage their own care; and establishing long-term clinical efficiencies. Life Sciences Venture Financings for WSGR Clients By Scott Murano, Partner (Palo Alto)

The data demonstrates that venture financing activity increased significantly during the first half of 2016 compared to the second half of 2015 with respect to the total amount raised and the number of closings. Specifically, the total amount raised across all industry segments increased 35.3 percent from the second half of 2015 to the first half of 2016, from $625.83 million to $847.05 million, while the total number of closings across all industry segments increased 63.1 percent, from 65 closings to 106 closings. Notably, the industry segment with the largest number of closings—medical devices and equipment—experienced an increase in both number of closings and total amount raised during the first half of 2016 compared to the second half of 2015. Specifically, the number of closings in medical devices and equipment increased 77.8 percent, from 27 closings to 48 closings, while the total amount raised in the segment increased 43.4 percent, from $215.73 million to $309.39 million. Similarly, the industry segment with the second-largest number of closings—biopharmaceuticals—experienced an increase in both number of closings and total amount raised: the number of closings increased 55 percent, from 20 closings to 31 closings, and the total amount raised increased 132 percent, from $181.21 million to $420.39 million. Meanwhile, the industry segment with the fourth-largest number of closings—diagnostics—also experienced an increase in both number of closings and total amount raised. Specifically, diagnostics experienced a 100 percent increase in number of closings, from four closings to eight closings, and a 14.6 percent increase in total amount raised, from $33.02 million to $37.84 million. All remaining industry segments (in descending order of number of closings)—digital health, genomics, and healthcare services—were up in number of closings but down in total amount raised during the first half of 2016 compared to the second half of 2015. In addition, our data suggests that Series A financing and bridge financing activity compared to Series B and later-stage equity financings and recapitalization financings increased during the first half of 2016 compared to the second half of 2015. Specifically, the number of Series A closings as a percentage of all closings increased from 29.2 percent to 31.8 percent, while the number of bridge financing closings as a percentage of all closings increased from 26.2 percent to 31.8 percent. Offsetting those gains, Series B financing, Series C and later-stage financing, and recapitalization financing activity compared to all other financings decreased during the first half of 2016. The number of Series B closings as a percentage of all closings decreased from 18.5 percent to 15.9 percent; the number of Series C and later-stage financing closings as a percentage of all closings decreased from 21.5 percent to 15 percent; and the number of recapitalization financing closings as a percentage of all closings decreased from 4.6 percent to 1.9 percent. Average pre-money valuations for life sciences companies decreased for Series A financings, but increased at later stages of financing during the first half of 2016 compared to the second half of 2015. The average pre-money valuation for Series A financings decreased 50.7 percent, from $22.04 million to $10.86 million; the average pre-money valuation for Series B financings increased 197.5 percent, from $35.36 million to $105.2 million; and the average pre-money valuation for Series C and later-stage financings increased 43.9 percent, from $84.07 million to $120.97 million. Other data taken from transactions in which all firm clients participated in the first half of 2016 suggests that life sciences is the third-most attractive industry for investment. For the first half of 2016, life sciences represented 22 percent of total funds raised by our clients, while the software industry—traditionally the most popular industry for investment—represented 23 percent of total funds raised. Services represented 28 percent of total funds raised. Overall, the data indicates that access to venture capital for the life sciences industry increased during the first half of 2016 compared to the second half of 2015. It is also worth noting that financing activity during the second half of 2015 had increased marginally over the first half of 2015, so the first half of 2016 marked the second straight six-month period of improved financing activity. Moreover, while activity during the second half of 2015 was concentrated around later-stage financings, activity during the first half of 2016 was concentrated around Series A and bridge financings—a welcome change for entrepreneurs who for so long have struggled to raise capital at the earlier stages. Of course, the improved early-stage financing activity does not come free, as evidenced by the decline in Series A pre-money valuations to more traditional levels.

WSGR Hosts 23rd Annual Phoenix Conference

On October 5-7, 2016, Wilson Sonsini Goodrich & Rosati hosted the 23rd annual Phoenix Conference at the Montage Laguna Beach in Laguna Beach, California. The exclusive event brought together 170 senior executives from large healthcare companies and CEOs of small, venture-backed firms for an opportunity to discuss critical issues of interest to the medical device sector, as well as to network and gain valuable insights from industry leaders and peers. The two-day conference featured presentations on a broad range of topics, including new sources of medtech funding, the identification of commercialization strategies, vulnerabilities in medical device companies risk assessment, medtech company exit strategies, and the 2016 elections implications for investors. The event also included a lunch featuring Bob Pearson, president of W2O Group, who discussed a new form of marketing called storytizing that enables companies to identify target audiences—whether theyre medical providers, advocates, patients, caregivers, or journalists—with precision. In addition, as part of the conferences Corporate Spotlight series, Bryan Hanson, EVP and president of Medtronics Minimally Invasive Therapies Group, offered insight into the opportunities and challenges that device companies currently face and the dynamics driving the industry. In connection with the event, the Phoenix Hall of Fame for Medical Device & Diagnostic Leadership celebrated the accomplishments of companies and individuals at a reception, dinner, and awards ceremony on the evening of October 6. NeoTracts UroLift System, which treats benign prostatic hyperplasia (BPH), was honored with the Most Promising New Product award, and Glaukos, an ophthalmic medical technology company focused on the development of products and procedures designed to treat glaucoma, was presented with the Emerging Growth Company award. Fred Khosravi, a Silicon Valley medical device entrepreneur, received the Phoenix Innovator Award, while William Link, Ph.D., co-founder and managing director at Versant Ventures, was named the Lifetime Achievement Award recipient. Recent Life Sciences Client Highlights

Sumitomo Dainippon Pharma to Acquire Tolero Pharmaceuticals

Biotech Board of Directors and Senior Executives Reception 25th Annual Medical Device Conference Phoenix 2017: The Medical Device and Diagnostic Conference for CEOs

Click here for a printable version of The Life Sciences Report This communication is provided as a service to our clients and friends and is for informational purposes only. It is not intended to create an attorney-client relationship or constitute an advertisement, a solicitation, or professional advice as to any particular situation. © 2017 Wilson Sonsini Goodrich & Rosati, Professional Corporation |

Steve Allan is the head of SVB Analytics, responsible for the three areas of information services provided to the innovation economy: Strategic Advisory Services, Compliance Valuations, and Insights. Strategic Advisory Services provides consultative guidance around valuations, benchmarking, and inorganic growth strategies. Compliance Valuations issues valuation opinions for private companies. Insight focuses on studying trends and opportunities in the private venture-backed innovation ecosystem. Steve brings a strong financial background and passion for entrepreneurship to his role at SVB Analytics.

Steve Allan is the head of SVB Analytics, responsible for the three areas of information services provided to the innovation economy: Strategic Advisory Services, Compliance Valuations, and Insights. Strategic Advisory Services provides consultative guidance around valuations, benchmarking, and inorganic growth strategies. Compliance Valuations issues valuation opinions for private companies. Insight focuses on studying trends and opportunities in the private venture-backed innovation ecosystem. Steve brings a strong financial background and passion for entrepreneurship to his role at SVB Analytics. Alex Lee is a valuation manager at SVB Analytics, responsible for conducting due diligence and financial analysis on valuation engagements for venture-backed companies in the life science sectors.

Alex Lee is a valuation manager at SVB Analytics, responsible for conducting due diligence and financial analysis on valuation engagements for venture-backed companies in the life science sectors.